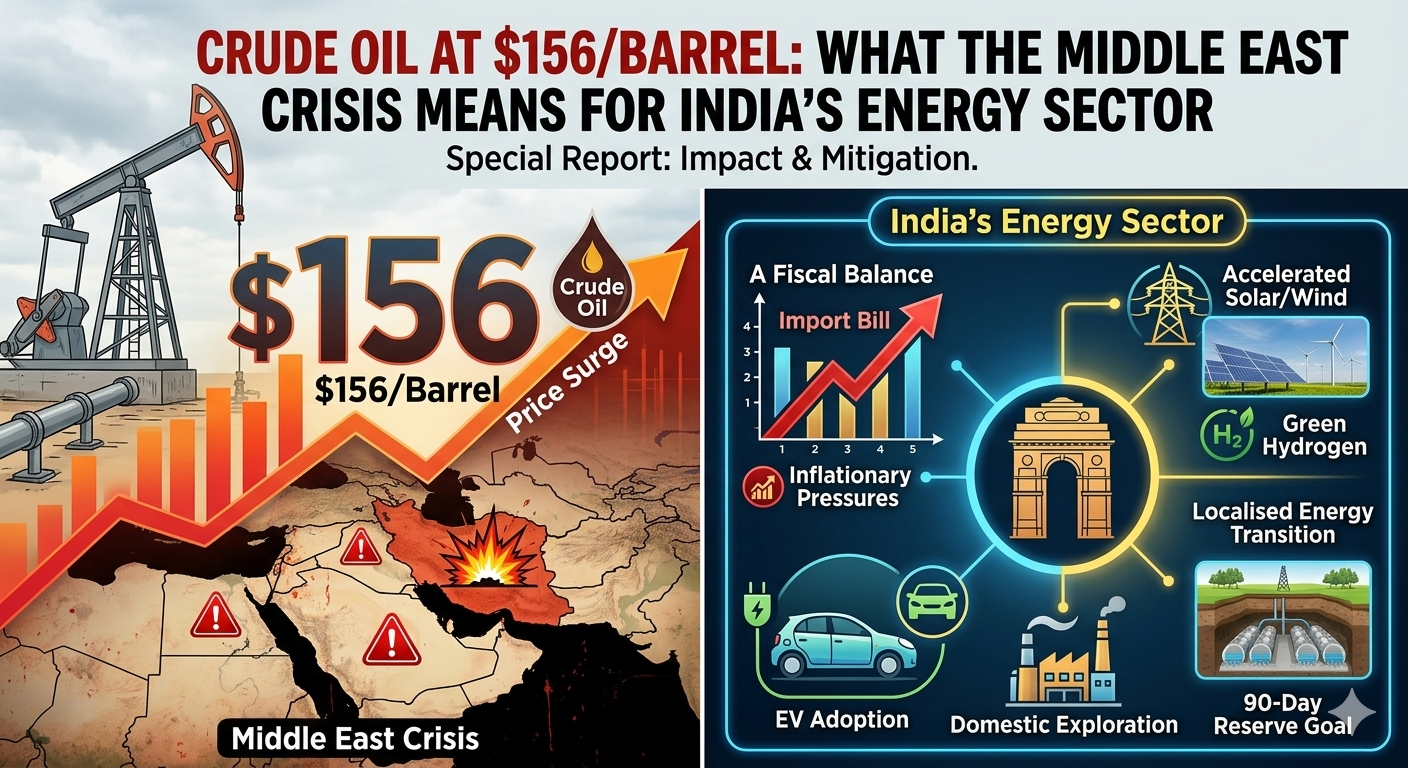

New Delhi, March 24, 2026 — India’s crude oil import basket surged to $156.29 per barrel on March 19 as the escalating Iran–US–Israel conflict disrupted Strait of Hormuz shipping lanes, sending shockwaves through India’s energy sector and raising the spectre of a widening current account deficit and government subsidy burden.

The Global Picture

Brent crude oil prices have climbed to the $106–112 per barrel range in March 2026, with the India basket — reflecting the weighted average cost of India’s actual crude import mix — peaking at $156.29/barrel on March 19 and having touched $146.09 on March 17. The surge is driven by the ongoing Iran–US–Israel military conflict, coordinated attacks on Gulf energy infrastructure, and severe congestion and risk premiums in the Strait of Hormuz, through which a significant share of global crude supply transits. Global energy markets have repriced supply risk sharply, with no immediate resolution in sight.

India’s Exposure

India imports approximately 85–90% of its crude oil requirements, making it among the most exposed large economies to global price shocks. At $156/barrel, India’s annual crude import bill could exceed ₹23–25 lakh crore ($280–300 billion), potentially widening the current account deficit to 1.9–2.2% of GDP from more manageable prior-year levels. The rupee has come under pressure against the dollar, amplifying the cost of imports further. India’s three major oil marketing companies — Indian Oil Corporation (IOC), Bharat Petroleum Corporation (BPCL), and Hindustan Petroleum Corporation (HPCL) — are absorbing the cost surge as retail petrol and diesel prices remain frozen to contain consumer inflation, leading to sharply compressed marketing margins and stock price declines of 20–25% over the past three weeks.

Sectors Most at Risk or Benefit

The oil price shock has created a sharp divergence across India’s industrial landscape:

- Upstream E&P (ONGC, Oil India): Direct beneficiaries — higher global crude realisations boosting revenues significantly; analysts estimate every $5/barrel rise adds 7–12% to EPS for upstream producers.

- Downstream OMCs (IOC, BPCL, HPCL): Under severe margin compression from unrecovered marketing losses; have suspended fuel supply on short-term credit to petrol pump dealers, requiring advance payments.

- Aviation & Road Logistics: IndiGo, SpiceJet and road freight operators face sharply higher jet fuel and diesel costs, squeezing operational margins and likely forcing fare revisions.

- Fertilisers & Petrochemicals: Rising hydrocarbon feedstock prices are threatening margins across the chemicals value chain, including agrochemicals, polymers and plastics manufacturers.

Outlook

India has meaningfully diversified its crude import basket to over 40 source countries, with approximately 70% of imports now routed outside the Strait of Hormuz — up from 55% earlier — providing partial insulation against a complete supply disruption. However, a sustained $100+ crude environment will test the government’s fiscal discipline and its capacity to avoid a subsidy-driven expenditure spike heading into FY2026-27. Any diplomatic breakthrough in West Asia — including the US–Iran talks signalled by President Trump — would be a significant positive catalyst for Indian markets, OMC stocks, the rupee, and broader industrial input cost relief.

— Industrial Front Desk

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment